How the American Education System Has Failed to Bridge the Gap to Financial Literacy

“The number one problem in today’s generation and economy is the lack of financial literacy.”

– Alan Greenspan, Former Chief of the Federal Reserve

University Graduates

“Upon entering the real world post-grad, I realized everyone around me, myself included, was financially planning for the present and not the future,” said Jack Goldman, a 2023 graduate from the University of Southern California.

Portrait of Jack Goldman. Citation below.

Jack Goldman was one of thousands of seniors to graduate from the University of Southern California in 2023, and one of millions of college graduates across the United States who were now tasked with entering the workforce. He graduated with a degree in Gerontology.

Upon graduating, he was presented with the difficulties of trying to acquire a post graduate job in an ailing economy. Despite this challenge, he secured a job as a Healthcare Analyst at an Investment Management firm.

He soon made the move to New York to start his job, where he quickly realized that securing a job is only the first hurdle in the journey to becoming financially independent. Investing, retirement savings, taxes, and credit cards all became pressing issues to which he had no previous exposure.

Financial Literacy Rates In America

Youtube video about financial literacy basics, created by author.

Despite going to a private, college preparatory school for high school, followed by a private university, Goldman was never exposed to the crucial lessons of personal finance. This is a fact that rings true for millions of Americans. In fact, there is a financial literacy crisis in America. According to the Ramsey Report from December 2023, 88% of adults say they left high school not being prepared to handle money in the real world. Additionally, a 2022 FINRA study found financial capability, stability, and confidence aren’t improving. Financial literacy is an issue across America, impacting people of all ages and backgrounds, that comes with a simple solution — improving education.

While there are many different levels of intricacy when it comes to financial literacy, there are some agreed upon basics that can significantly improve the financial well-being of millions of Americans if taught in schools. These include basics savings, emergency funds, credit scores/credit cards, loans, debt, and investing.

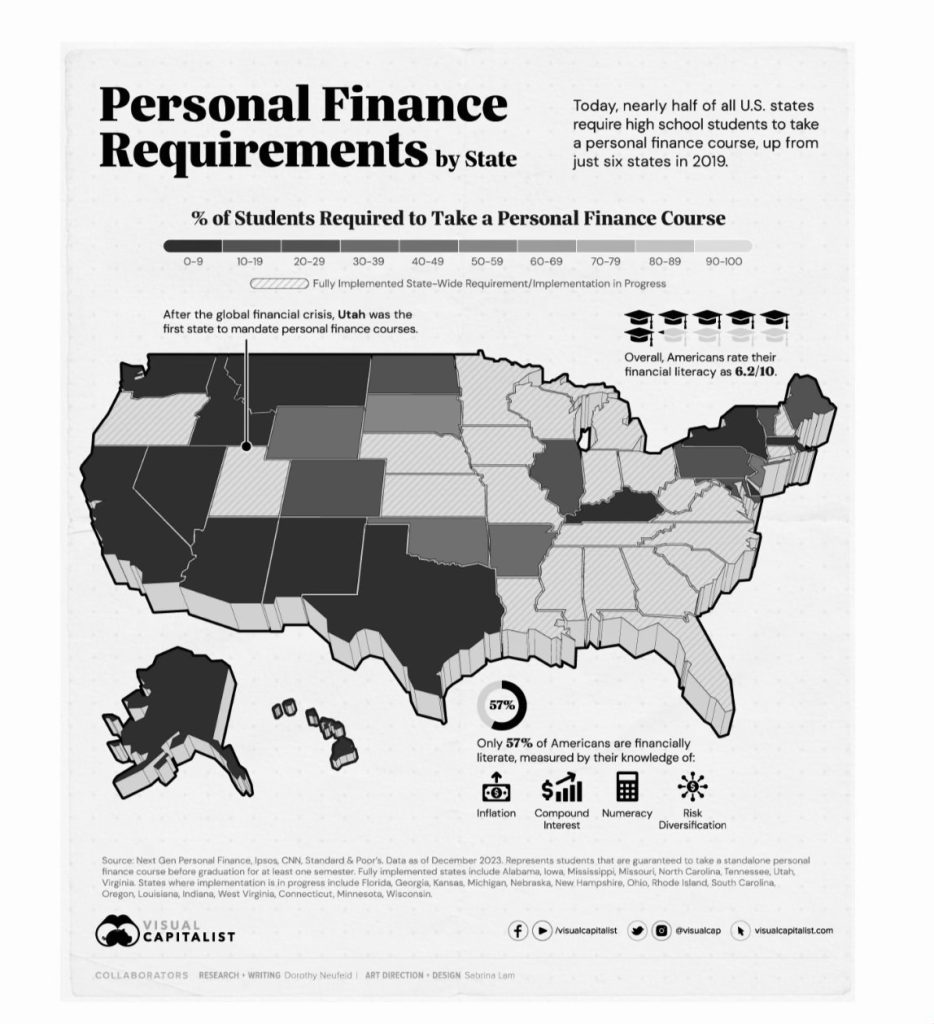

Personal finance requirements by state. Citation Below.

The pandemic revealed glaring financial issues across the United States, including income inequality, inflation, and student loan payments. As a result, certain states are beginning to require financial literacy classes in high school. These courses cover topics such as budgeting, saving, and managing debt. However, across the United States, just seven states (Alabama, Iowa, Mississippi, Missouri, Tennessee, Utah and Virginia) require students to take a semester-long personal finance course. The level of education on financial literacy varies by state, city, and county, and in many states under 10% of students are required to take a personal finance course.

While the conversation of what should be taught in the classroom can often be divisive across states, political parties, and religious groups, there appears to be a state of agreement that financial literacy is something that should be taught in the classroom. According to a 2022 poll from the National Endowment for Financial Education 88% of adults said their state should require a semester or year-long financial education course for graduation.

Crippling Student Debt

Tik Tok highlighting normalization of student debt. Citation below.

When it comes to important financial topics, student debt is one of the biggest issues. According to the federal reserve, as of the third quarter of 2023, Americans owed $1.74 trillion in education debt. 51% of 2021-22 bachelor’s degree recipients graduated with an average of $29,400 in student loan debt. Among all borrowers, the average student loan debt in 2023 was $38,290. Student loan debt is now the second highest consumer market behind mortgages.

While student loans are a valuable tool, many young adults don’t understand the impact and commitment when making a college decision at age 18. Additionally, social media trends have allowed student loan debt to become something that is glamorized.

Within the last month alone, a new trend has swept across Tik Tok where young students talk about attending schools like UGA or College of Charleston, only to accumulate a six figure student loan debt, while romanticizing factors like the beach or game day making the financial commitment worth it.

As people continue to use social media to romanticize student debt, without a genuine understanding of how interest accumulates and how long a payoff plan could potentially take, more individuals may take on financial commitments that they are unprepared for. It is important to have a good understanding of whether or not family can contribute, what your interest rates look like, estimations for monthly payments, and common salaries for your specific degree. While social media can be a powerful educational tool, it has the power to mislead. Financial information and education should always come from verified sources.

Resources like federal student aid will always be less expensive in comparison to private student loans. Private student loans can also be a powerful tool, but it is good to shop around for the best rates and avoid taking out too many private student loans. Regardless, one rule of thumb for student debt is that you should try not to borrow more than the first year salary you can expect in your chosen field.

Trevor Dorman throwing his graduation cap. Citation Below.

Trevor Dorman is a current senior at the University of Southern California, where he is studying business. Despite USC being his top choice, he also made the decision to come because after financial aid had been taken into account, USC was one of his most affordable options. Despite this being the case, he takes out both federal and private student loans each year to cover tuition, rent, and living expenses.

“One of my biggest concerns for post-grad is figuring out a plan to quickly pay off the student debt I have accumulated over the last few years. Despite being far from six figures of student debt, cost of living is so high in our current economy that it is hard to find an entry level job with a salary sufficient enough to cover life expenses, plan for the future, and pay off debt,” said Dorman.

As more and more students are influenced by the glamorization of universities and the normalcy of six figure student debt for an undergraduate degree, it is essential for people to learn basic principles in regard to interest, and how long that level of debt would take to pay off on an entry level post-grad salary. Student debt can quickly become a lifelong burden, and because it is so normalized, often people do not understand the significance of their financial commitment before it is too late.

High school students should be educated on federal and private loans, as well as the difference in financial aid policies for public and private universities. This will allow them to make more educated decisions about college, both when applying as well as choosing the best school for them.

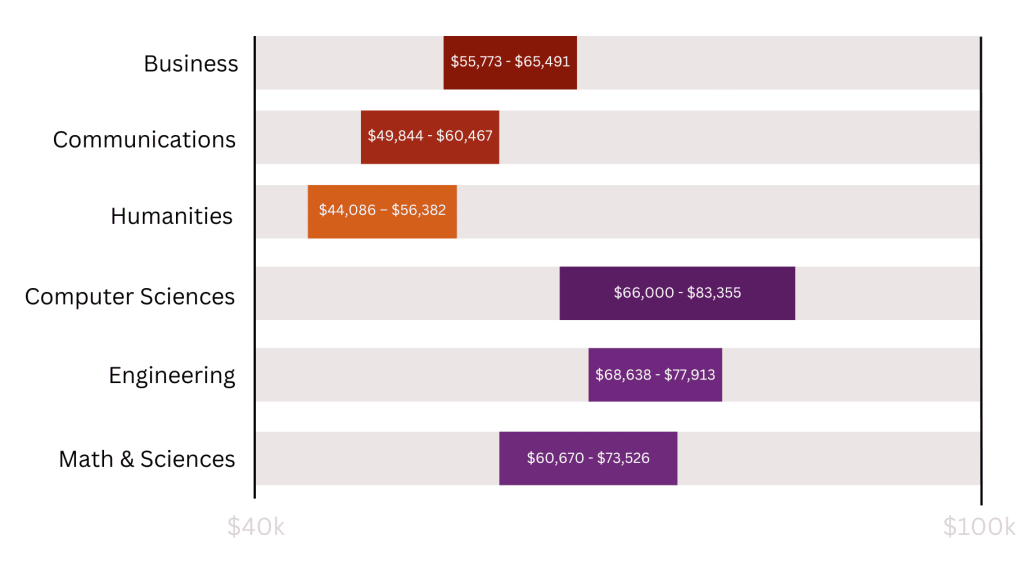

In the state of California, the median salary for college graduates is around $63,000 (the 6th highest of all 50 states). According to Forbes, paying off a $100,000 student loan debt with a payment of $1000 per month would take 120 months, or ten years. Not only is this over a decade of paying off loans, but for those with a 60k salary in the state of California, they can expect to see a net pay of 3800 a month. If an individual were expecting to pay one grand for rent, and one grand on student debt per month, this is over half of one’s salary gone every month for the next decade. Salary expectations also have to be considered based on a degree, as some majors like engineering or computer science have much higher starting salaries, swaying the median salary upwards.

Graph highlighting starting salaries by major. Citation below.

Willa Dorgan, a senior at The University of Southern California, chose to pursue a degree in economics because of job and financial stability. She felt that choosing another major such as environmental science, which is more in line with her passions and interests, would equate to significant risk down the line. She spent her summer interning as a consultant for KPMG, a global accounting and consulting firm.

Willa Dorgan at KPMG Lakehouse. Citation below.

“I feel we live in a world where people press the importance of a college degree. However, I also feel we have gotten to the point where the cost of a degree is not worth the job opportunities in all industries. While this isn’t a traditional aspect of financial literacy people consider, it is important for people to be aware of job opportunities based on their degree,” said Dorgan. “A $200,000 degree is not always worth the job opportunities it results in.”

Higher Level Education and Financial Literacy

While student loan debt is a serious problem that lacks an educational foundation in America, it is only one of many topics not taught that is impacting the financial wellbeing of students and individuals across America. Lori Shreve Blake is the Senior Director of Career Engagement at USC. She has worked at USC for the last 24 years where she tries to help students enter the workforce. Every year she organizes a financial literacy conference to help educate USC students.

Graph representing financial literacy responses by age. Citation below.

“Despite being at one of the top universities in the United States, it is shocking how little many students know about financial literacy. It is often not taught in high school or college, and people enter the workforce with little to no idea of how to plan for financial Freedom,” said Blake. “With just a few basic concepts under one’s belt, such as saving for retirement and learning to invest, people can change their financial future.”

Lori Shreve Blake helped to highlight the concept that many economic experts have outlined, pertaining to the time value of money when it comes to saving and investing. Nearly half of America has reported having little to no retirement savings, yet basic plans can set one up for success. Blake emphasized the importance of a 401K rather than basic retirement savings, as a $100 monthly contribution to a 401K starting at age 25 with a 3% match from an employer would become nearly half a million dollars by the time one reaches retirement age.

“The reality is, the current education system has failed so many. There are so many education requirements in place starting at a young age, but one of the most useful and impactful tools (financial literacy), is not properly taught.”

Lori Shreve Blake, Senior Director of Career Engagement at USC

Racial Inequality and Financial Literacy

Average US family net worth by race. Citation below.

While a lack of financial literacy affects all communities, its impact is not felt equally. Levels of financial literacy are in fact much lower among Black and Hispanic Americans than White and Asian Americans. FINRA, the Financial Industry Regulation Authority, released a national study in 2018 highlighting these issues. According to the study, in an assessment of basic financial literacy, Asian and White Americans answered an average of 3.6/6 questions correctly, Hispanic Americans answered an average of 2.6 correct, and Black Americans answered an average of 2.3 correct. Furthermore, according to this study two of the main factors contributing to a young individual’s financial literacy is household income and education, further pointing back to the significant racial wealth gap that continues to permeate our society and impact future generations.

This wealth gap isn’t a direct reflection of education levels, as “Black families whose head earned a college degree is only about two-thirds of the median wealth of White families whose head dropped out of high school.” Rather, these issues stem from political and social barriers dis-valuing minority communities. Employing mandatory financial literacy classes in schools may be used as a step forward in the financial literacy crisis and racial wealth gap to begin leveling the playing field across racial communities.

Need For Curriculum Reform

USC Scholars of Finance 2024 Symposium. Citation Below.

Rebecca Flynn is another current student at The University of Southern California who works as one of the Vice Presidents for USC Scholars of Finance. Her interest in personal finance came from her parents, as she pointed out that she never received formal schooling about personal finance in high school or college.

“My knowledge base is something I sought out after being influenced by my parents,” said Flynn. “For so many, they don’t have the privilege of having parents well informed on financial literacy, and as a result could go their entire life without ever learning these essential concepts. Even through concepts as simple as knowledge we can continue to see long-term wealth gaps become further and further exasperated.”

Despite being a part of a club that focuses particularly on finance and careers in finance, Flynn shared that there is a surprising lack of knowledge on personal finance, even when it comes to groups of those interested in careers in finance. This interesting juxtaposition highlights the way in which personal finance and awareness around the subject is continuing to suffer.

“The American education system has failed so many, and no one recognizes it. If even some of the most privileged students in America haven’t learned these basic concepts, we cannot expect those without generational wealth and knowledge to succeed without support and changes to our curriculum as a nation,

Rebecca feng, USC Student

Citations Jack Goldman portrait provided by Jack Goldman. Personal finance requirements by state map from Visual Capitalist. Tik Tok via @babylena_ on Tik Tok. Trevor Dorman portrait provided by Trevor Dorman. Salary by major graph from Wells Fargo. KPMG Lakehouse image provided by Willa Dorgan. Financial literacy percentile graph from CivicScience. Black and Hispanic wealth gap graph from Statista. USC Scholars of Finance image provided by club.